In a high-interest environment like 2025, finding the best high-yield savings accounts in the U.S. 2026 can make a meaningful difference in how fast your money grows. With annual percentage yields (APYs) surpassing 5.00%, many online banks and fintech institutions now offer returns that easily outpace traditional savings options. Whether you’re saving for emergencies, short-term goals, or simply want a smarter way to grow idle cash, this guide highlights the top-performing accounts of the year based on APY, accessibility, and customer satisfaction.

Read Also: Best High-Yield Savings Accounts in the USA for 2026

What Is a Savings Account?

A savings account is an account at a bank or credit union that is designed to hold your money. Savings accounts typically pay a modest interest rate, but they are considered safe for parking cash that you want available for short-term needs.

Some savings accounts pay a higher yield than other savings accounts.1 They may have some limitations on how often you can withdraw funds. Generally, savings accounts offer flexibility that can be ideal for building an emergency fund, saving for a short-term goal like buying a car or going on vacation, or simply earning a little interest on your savings.

Key Takeaways

- Savings accounts are bank or credit union accounts designed to keep your money safe while paying interest.

- Your savings account funds will be easily accessible, which can be an ideal option for emergency funds.

- You’ll typically earn a lower rate in savings accounts versus other options like CDs or bonds.

- The interest you earn on a savings account is considered taxable income.

How Savings Accounts Work

Savings and other deposit accounts are secure bank accounts used to store your funds while potentially earning interest.

For banks, they are important sources of funds for lending. For that reason, you can find savings accounts at virtually every bank or credit union, whether they are traditional brick-and-mortar institutions or operate online. In addition, some investment and brokerage firms offer savings accounts.

Savings account interest rates vary. With the exception of promotions promising a fixed rate until a certain date, banks and credit unions might change their rates at any time. Typically, the more competitive the rate, the more likely it is to fluctuate.

Changes in the federal funds rate can trigger institutions to adjust their deposit rates.2 Some institutions offer high-yield savings accounts with significantly higher interest rates for larger minimum deposits, which may be worth investigating.

Savings Account Rules

Some conventional savings accounts require a minimum balance to avoid monthly fees or earn the highest published rate, while others have no balance requirement. Know the rules of your particular account to ensure you avoid diluting your earnings with fees.

Money can be transferred in or out of your savings account online, at a branch or ATM, by electronic transfer, or by direct deposit. Transfers can usually be arranged by phone, as well.

Some banks limit withdrawals to six per month. If you exceed that, the bank may charge a fee, close your account, or convert it to a checking account. The amount you can withdraw is unlimited, so you can withdraw up to the amount in the account.3

Just as with the interest earned on a money market, certificate of deposit, or checking account, the interest earned on savings accounts is taxable income.

The financial institution where you hold your account will send a 1099-INT form at tax time whenever you earn more than $10 in interest income. The tax you’ll pay will depend on your marginal tax rate.4

Top High-Yield Savings Accounts in the U.S. 2026

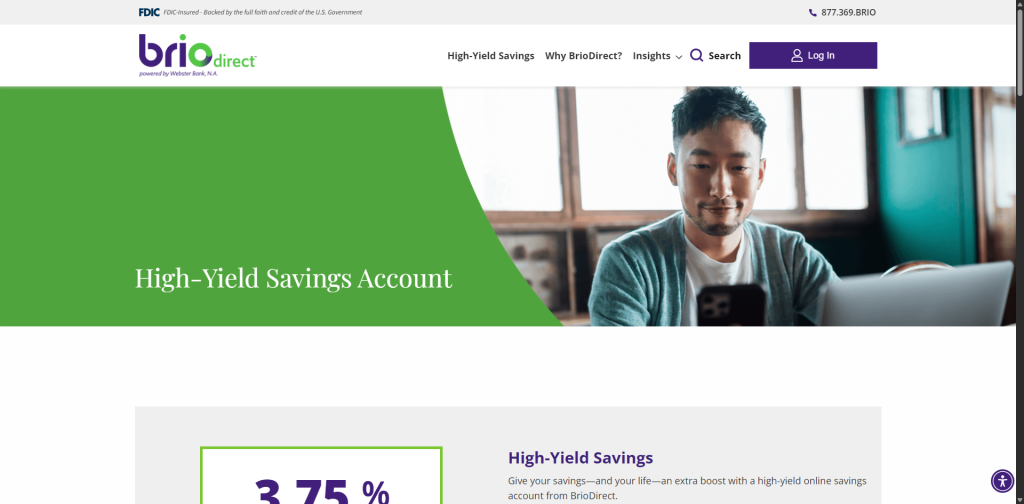

1. BrioDirect High-Yield Savings Account

- APY: 5.30%

- Minimum Deposit: $5,000

- Monthly Fees: None

- Why It Stands Out: Offers one of the highest yields in 2025, ideal for savers with a solid initial deposit. Perfect for maximizing passive income from cash reserves.

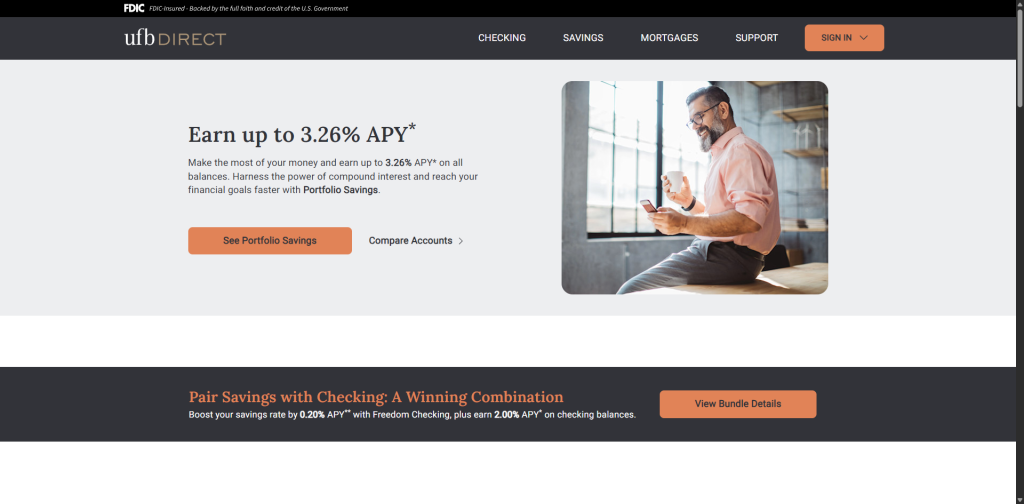

2. UFB Direct High-Yield Savings

- APY: 5.15%

- Minimum Deposit: $0

- Monthly Fees: None

- Why It Stands Out: High interest plus no minimum makes this account perfect for new savers and seasoned investors alike. Comes with optional ATM access.

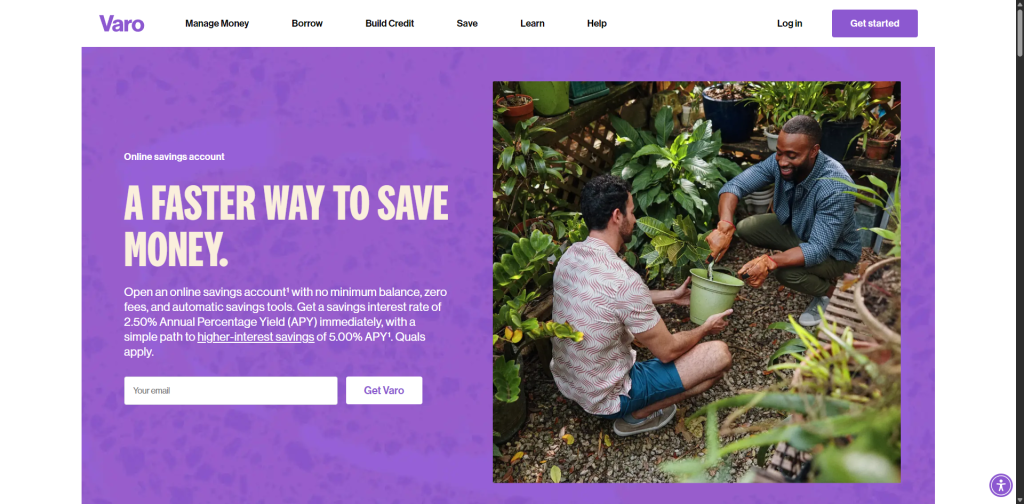

3. Varo Bank Savings Account

- APY: Up to 5.00%

- Minimum Deposit: $0

- Monthly Fees: None

- Why It Stands Out: Competitive tiered APY structure that rewards consistent deposits and healthy balances. Great mobile app and digital banking tools.

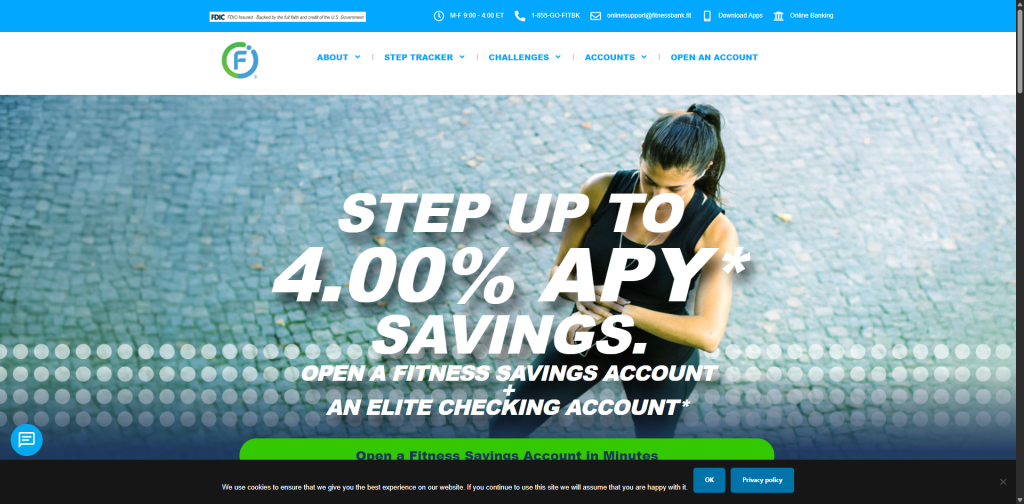

4. FitnessBank Savings Account

- APY: 5.00%

- Minimum Deposit: $100

- Monthly Fees: None

- Why It Stands Out: Unique model links your APY to your step count. Combines financial wellness with physical activity—ideal for health-conscious savers.

5. Pibank High-Yield Savings

- APY: 4.60%

- Minimum Deposit: $0

- Monthly Fees: None

- Why It Stands Out: Easy to open, no-frills account with strong interest and minimal barriers. Great for beginners and anyone seeking low-maintenance savings.

Why Choose a High-Yield Savings Account?

High-yield savings accounts are an excellent vehicle for parking your money while earning interest above inflation. They’re safe, flexible, and typically insured by the FDIC up to $250,000. Whether you’re preparing for a big purchase or building your emergency fund, these accounts allow your money to grow while remaining liquid. Unlike CDs or stocks, there’s no risk of capital loss or penalty for early withdrawal.

Key Features to Compare Before Opening an Account

To choose the best high-yield savings account in the U.S. 2025, compare accounts based on:

- APY: Higher rates yield more interest over time.

- Fees: Look for zero monthly maintenance fees.

- Minimum Balance Requirements: Ensure you meet any minimums to avoid reduced rates.

- Customer Support & Digital Experience: Top accounts come with mobile apps, helpful customer service, and seamless transfers.

- Compounding Frequency: Daily compounding earns more than monthly.

Tips to Maximize High-Yield Savings Benefits

- Automate Deposits: Build your savings habit without thinking about it.

- Keep Your Emergency Fund There: It grows without locking your money up.

- Use for Short-Term Goals: Whether it’s a vacation, car, or new laptop, keep your goal-focused savings separate.

- Monitor Rate Changes: APYs are variable, so stay informed and switch banks if needed.

Pros of Savings Accounts Explained

- Easy to use: Holding a savings account at the same institution as your primary checking account can offer several benefits, such as convenience and efficiency. Because transfers between accounts at the same bank are usually instantaneous, deposits or withdrawals to your savings account from your checking account will take effect right away.

- Can be linked to checking account: Linking your checking and savings account makes it easy to transfer excess cash from your checking account and have it immediately earn interest. Or you may want to transfer money from your savings to cover a large checking transaction.

- Withdraw balance at any time: Your access to funds in a savings account will remain extremely liquid, unlike certificates of deposit, which impose a hefty penalty if you withdraw your funds too soon.

- Up to $250,000 is federally insured: Federal protection against bank failures provided by the Federal Deposit Insurance Corp. (FDIC) will keep your money safer than it would be under your mattress or in your sock drawer.5

Cons of Saving Accounts Explained

- Pays less interest than other options: The trade-off for a savings account’s easy access and reliable safety is that it won’t pay as much as other savings instruments. You can usually earn a higher return with certificates of deposit or Treasury bills, or by investing in stocks and bonds, if your time horizon is long enough.

- Easy access can make withdrawals tempting: The availability of funds may tempt you to spend what you’ve saved.

- May require minimum balance: Certain savings accounts request a minimum balance to avoid monthly fees or earn the highest published rate.

How to Maximize Earnings From a Savings Account

Although most major banks offer low interest rates on their savings accounts, many banks and credit unions provide much higher returns. In particular, online banks offer some of the highest savings account rates. Because they don’t have physical branches—or have very few—they spend less on overhead and can often offer higher, more competitive deposit rates as a result.

The key is to shop around, starting with the bank where you hold your checking account. Even if that institution doesn’t offer a competitive savings account rate, it will give you a frame of reference for how much more you can earn by moving your savings or opening an additional account elsewhere.

As you shop for the best rates, however, beware of account features that can curtail your earnings, or even drain them. Some promotional savings accounts will only offer the attractive rate they’re advertising for a short period of time.

Others will cap the balance that can earn the promotional rate, with dollar amounts above that maximum earning a paltry rate.6 Even worse is a savings account with fees that cut into the interest you earn each month.

How to Open a Savings Account

To set up a savings account, visit one of the bank or credit union’s branches, or establish the account online, for those institutions that offer it. You’ll need to provide your name, address, and telephone number, as well as photo identification. Also, because the account earns taxable interest, you’ll need to provide your Social Security number (SSN).7

Some institutions will require you to make an initial minimum deposit at the time you open the account in order to receive account opening bonus. Others will allow you to open the account first and fund it later.

How Much to Keep in Your Savings Account

The amount you keep in your savings account will depend on your goals for the funds, or your use of the account.

If you’ve set up the savings account to sweep excess funds from your checking account, your balance is likely to vary regularly. In contrast, if you are building up to a savings goal, your balance will likely start low and increase steadily over time.

If your savings account is your emergency fund, aim for enough to cover at least three to six months’ living expenses. That gives you some financial cushion if you face an unexpected expense like a medical or car repair bill or if you lose your job.

Depending on your financial situation, you may want to keep some of that emergency fund in a simple savings account, and invest the rest to seek higher returns.

Keep in mind that up to $250,000 of your deposits are protected by FDIC insurance or NCUA insurance. That ensures your funds are safe should the institution fail. For most consumers, this more than covers what they have on deposit. But if you are holding more than $250,000 in deposit accounts, consider splitting your balance across more than one account holder or institution.85

Kids and Student Savings Accounts

You must be at least 18 or over to open a savings account on your own in the U.S., though this requirement can vary by state9 But many savings accounts are designed for minors. You can get a savings account for a child by co-signing for the account.

Bank accounts designed for students usually have maximum age restrictions. For example, you may not be able to open a student bank account if you are over 25. These accounts, designed to teach younger adults how to use a bank account, usually have lower fees and requirements, but they also tend to offer lower interest rates.

Read Also: M-Chama Groups Savings Account: Secure, Transparent Banking for Chamas

Frequently Asked Questions (FAQs)

How Do You Open a Savings Account?

You can open a savings account by visiting a bank branch with your government-issued ID and any cash or checks you wish to deposit. You will also be asked for your address, contact information, and a Social Security number or taxpayer identification number (TIN). You may have to open a checking account as well as a savings account, and there may be a minimum deposit threshold. It is also possible to open a savings account with an online bank.

What Savings Account Will Earn You the Most Money?

Savings account rates change often, so it is worth taking the time to compare the offerings from different banks and credit unions. As of June 2024, the best savings rates ranged from about 4.5% to 5.5%.

How Do You Close a Savings Account?

Most banks allow three ways to close an account. You can either visit the bank in person, submit a written cancellation request form, or close the account over the phone. In each case, you may be asked to provide identifying information.

Conclusion

Choosing the best high-yield savings accounts in the U.S. 2025 empowers you to take control of your financial future. With APYs well above the national average and accounts offering zero fees and easy access, there’s no reason to let your money sit idle in a low-interest account. Evaluate your goals, compare features, and take advantage of the high-interest era to make every dollar work harder for you.

References:

- NerdWallet: https://www.nerdwallet.com/best/banking/high-yield-online-savings-accounts

- Forbes: https://www.forbes.com/advisor/banking/savings/best-high-yield-savings-accounts

- Bankrate: https://www.bankrate.com/banking/savings/best-high-yield-interests-savings-accounts

- Investopedia: https://www.investopedia.com/best-high-yield-savings-accounts-4770633

- Business Insider: https://www.businessinsider.com/personal-finance/banking/best-high-yield-savings-accounts-rates-right-now

- Best High-Yield Savings Accounts in the U.S. 2025

{kind=link}