Compound interest is one of the most powerful concepts in finance because it allows your money to grow not only on the original deposit but also on the interest already earned over time. Learning how to calculate compound interest can help you better understand investments, savings accounts, loans, and long-term wealth building.

Compound interest is interest accumulated from a principal sum and previously accumulated interest. It is the result of reinvesting or retaining interest that would otherwise be paid out, or of the accumulation of debts from a borrower.

Read Also: Forex Trading in Kenya: What Drives Interest and What Traders Should Understand

Compound interest is contrasted with simple interest, where previously accumulated interest is not added to the principal amount of the current period. Compounded interest depends on the simple interest rate applied and the frequency at which the interest is compounded.

Unlike simple interest, which is only calculated on the principal amount, compound interest continuously increases because interest keeps accumulating on previous interest earnings. This process is often called:

- “interest on interest”

and it can dramatically increase the future value of money over long periods.

What Is Compound Interest?

Compound interest is the interest calculated on:

- The original principal

- Previously earned interest

This means the balance grows faster over time compared to simple interest.

For example:

- If you save money in a bank account with compound interest, the account balance increases more rapidly because every interest payment becomes part of the new balance used for future calculations.

According to financial experts, compounding is one of the key drivers behind long-term investment growth.

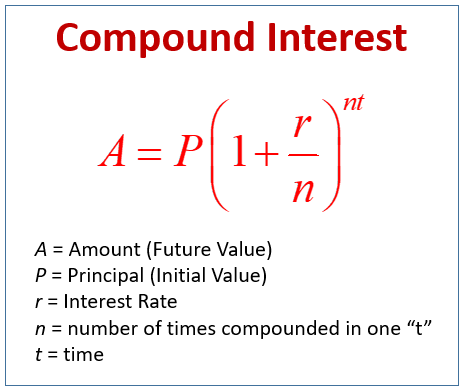

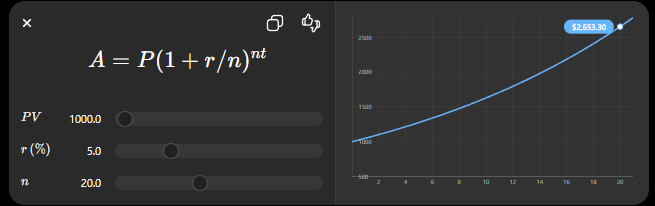

Compound Interest Formula

To calculate compound interest, use the following formula:

Where:

- A = Final amount

- P = Principal amount

- r = Annual interest rate (decimal form)

- n = Number of times interest compounds per year

- t = Time in years

To calculate only the compound interest earned:

CI=P(1+r/n)nt−P

Where:

- CI = Compound interest earned

Read Also: Pinterest Fires Engineers for Tracking Layoff Victims Using Custom Scripts

Step-by-Step Example

Let’s calculate compound interest using a practical example.

Example

You invest:

- $5,000

at an annual interest rate of:

- 5%

compounded monthly for:

- 3 years

Step 1: Identify Variables

- P = 5000

- r = 0.05

- n = 12

- t = 3

Step 2: Insert Values Into Formula

A=5000(1+0.05/12)12⋅3

Step 3: Calculate Final Amount

The investment grows to approximately:

- $5,808.08

Step 4: Find Compound Interest Earned

- $5,808.08 − $5,000

- = $808.08

So the compound interest earned is:

- $808.08

Why Compound Interest Grows Faster

Compound interest accelerates because each interest payment increases the principal balance.

For example:

Year 1

- Principal = $1,000

- Interest at 6% = $60

- New balance = $1,060

Year 2

- Interest is now calculated on $1,060

- Interest earned = $63.60

Year 3

- Interest calculated on $1,123.60

- Interest earned = $67.42

Each year, the interest grows larger because the balance keeps increasing.

Compound Interest vs Simple Interest

Simple Interest

Simple interest only applies to the original principal.

Formula:

SI=P⋅r⋅t

Compound Interest

Compound interest applies to:

- Principal

- Accumulated interest

This leads to significantly higher long-term returns.

Types of Compounding Frequency

The frequency of compounding greatly affects how fast money grows.

Annual Compounding

Interest compounds once per year.

Monthly Compounding

Interest compounds 12 times per year.

Daily Compounding

Interest compounds every day.

Continuous Compounding

Theoretical maximum compounding frequency.

The more frequently interest compounds, the greater the final amount becomes.

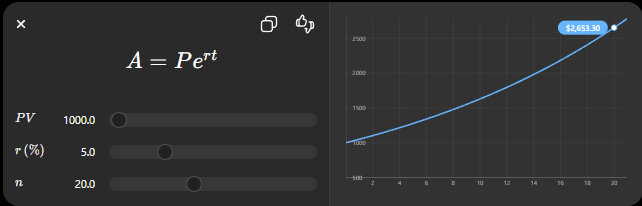

Continuous Compound Interest Formula

For continuous compounding:

Where:

- e = Euler’s number (~2.71828)

This formula calculates the maximum possible growth through constant compounding.

Real-Life Uses of Compound Interest

Learning how to calculate compound interest is important for:

Savings Accounts

Banks often offer compound interest on deposits.

Investments

Stocks, bonds, and retirement accounts benefit heavily from compounding over time.

Loans and Credit Cards

Compound interest can also work against borrowers by increasing debt balances faster.

Retirement Planning

Long-term retirement investing relies heavily on compound growth.

Compound Interest and Time

Time is one of the most important factors in compound growth.

The longer money remains invested:

- The greater the compounding effect

Even small amounts can grow significantly over decades.

For example:

- $10,000 invested at 8% annually for 30 years grows far beyond the original deposit because of compounding.

Compound Interest and Inflation

One major reason investors seek compound interest is to help outpace inflation.

Keeping money in low-interest accounts may reduce purchasing power over time.

High-yield savings accounts and long-term investments often provide stronger compounding returns.

Using Excel to Calculate Compound Interest

Compound interest calculations can also be done easily in spreadsheet software like:

- Microsoft Excel

- Google Sheets

Example Excel formula:

=P*(1+r/n)^(n*t)This automatically calculates future investment value.

Common Compound Interest Mistakes

Ignoring Compounding Frequency

Monthly compounding produces different results than annual compounding.

Forgetting Decimal Conversion

Interest rates must be converted from percentages to decimals.

Example:

- 5% = 0.05

Underestimating Time

Longer investment periods dramatically increase growth.

Final Thoughts on How to Calculate Compound Interest

Understanding how to calculate compound interest is essential for building wealth, managing debt, and making smarter financial decisions.

Compound interest allows money to grow exponentially over time because earnings continually generate additional earnings. Whether saving for retirement, building an emergency fund, or investing long-term, mastering compound interest can significantly improve financial outcomes.

The earlier you begin saving and investing, the more powerful compound interest becomes over time.

Read Also: Reversal of Erroneous Penalties and Interests on iTax Now Made Easier

{kind=link}