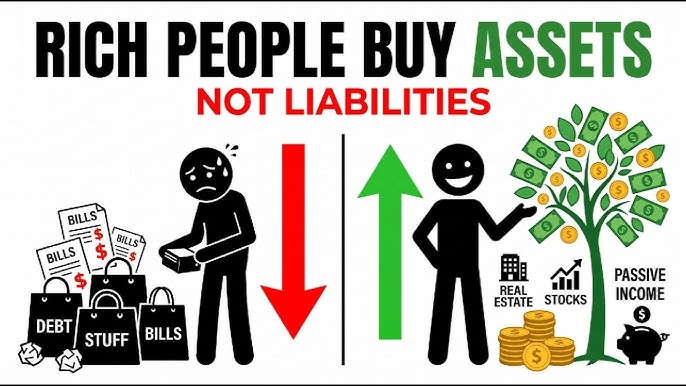

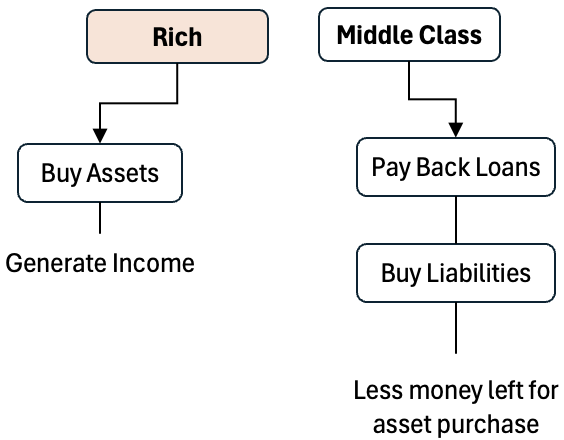

Wealthy people do not normally become wealthy simply by earning high incomes.

Income can support a comfortable lifestyle, but lasting wealth depends on what remains after spending and where that money is placed.

A person can earn a large salary and still own very little if every increase in income is used to finance a more expensive lifestyle. Another person may earn less but gradually build wealth by purchasing assets that grow, produce income or increase earning capacity.

This is the central difference between income and ownership.

Income is money received from work, business activities or investments. An asset is something with economic value that may generate income, appreciate, reduce future expenses or support the creation of additional value.

Wealthy investors often own a mixture of assets rather than depending on one salary, one property or one company.

Investor.gov explains that asset allocation involves dividing investments among categories such as stocks, bonds and cash. The appropriate mixture depends on factors including the investor’s time horizon and tolerance for risk.

The objective is not to purchase every asset on this list.

Some require substantial money, specialist knowledge or the ability to tolerate major losses. Others are accessible to ordinary investors through regulated funds or retirement accounts.

No asset is guaranteed to become profitable.

Property prices can fall. Companies can fail. Bonds can default. Intellectual property may produce no meaningful revenue. Private investments can be difficult to sell.

The useful lesson is that wealthy people often direct surplus income toward ownership rather than consumption.

Here are 10 assets commonly used to build, generate and preserve wealth.

1. Businesses

Business ownership is one of the most powerful wealth-building assets because it can create income, employment, intellectual property and an organisation that may eventually be sold.

A business owner can earn money through:

- Salary.

- Profit distributions.

- Dividends.

- Increased business value.

- Licensing.

- Franchising.

- Selling part or all of the company.

An employee is normally paid for work performed during a specific period.

A business owner may build systems, products and customer relationships that continue generating revenue beyond the owner’s individual working hours.

This does not make business income passive.

Most businesses require significant effort, capital, planning and risk. Many produce inconsistent profits, and some fail completely.

Successful owners create value by solving a customer problem profitably.

Examples include:

- Manufacturing.

- Media businesses.

- Software companies.

- Professional services.

- Retail operations.

- Logistics.

- Healthcare services.

- Construction.

- Education businesses.

- Food production.

- Financial services.

- Property management.

A business becomes more valuable when it has:

- Reliable revenue.

- Strong profit margins.

- Repeat customers.

- Valuable contracts.

- Recognisable branding.

- Effective management.

- Documented processes.

- Intellectual property.

- Low dependence on one employee or client.

A self-employed job is not automatically a valuable business asset.

When revenue stops completely whenever the owner stops working, the operation may have limited value to a buyer.

Wealthy entrepreneurs often focus on building systems that can function with a wider team.

Main risks of business ownership

Business ownership can involve:

- Loss of invested capital.

- Debt.

- Competition.

- Legal disputes.

- Changing customer demand.

- Employee problems.

- Regulation.

- Tax complexity.

- Cybersecurity threats.

- Economic downturns.

A business should not be started merely because entrepreneurship is presented as a fast route to wealth.

It should be based on a real market need, realistic costs and the owner’s ability to manage uncertainty.

2. Diversified stock funds

Stocks represent ownership in companies.

When an investor purchases shares, the investor becomes a partial owner of the underlying business.

Returns may come from:

- An increase in the share price.

- Dividends.

- Share repurchases that increase each remaining shareholder’s ownership percentage.

- Long-term company growth.

Wealthy investors may own individual companies, but many also use diversified mutual funds and exchange-traded funds.

A mutual fund pools money from many investors and can invest in stocks, bonds, money-market instruments and other assets.

A broad-market index fund may hold hundreds or thousands of companies.

This reduces the damage caused by the failure of one business.

Investor.gov explains diversification with the principle of not putting all one’s eggs in one basket. It also warns that diversification cannot guarantee protection against market losses.

Why wealthy people buy stock funds

Diversified funds can provide:

- Ownership in many businesses.

- Long-term growth potential.

- Dividend income.

- Liquidity.

- Relatively low minimum investments.

- Automatic diversification.

- Access to domestic and international markets.

They are also easier to manage than personally operating hundreds of companies.

Main risks of stock funds

Stock funds can decline sharply during:

- Recessions.

- Financial crises.

- Wars.

- Interest-rate changes.

- Technology disruptions.

- Periods of market panic.

Investors may lose money, particularly when forced to sell during a downturn.

Funds also charge fees. Even small annual charges can reduce long-term returns when compounded over decades.

Investors should examine:

- Expense ratio.

- Trading costs.

- Fund strategy.

- Index tracked.

- Geographic exposure.

- Concentration.

- Tax treatment.

- Currency risk.

The wealthy do not necessarily avoid market declines. They often manage the risk by maintaining long time horizons, sufficient liquidity and diversified holdings.

3. Individual company shares

Some wealthy investors buy direct ownership stakes in particular public companies.

This allows them to concentrate money in businesses they believe have strong competitive advantages, capable management and attractive growth prospects.

Individual shares can produce significant wealth when the company succeeds.

However, concentration magnifies both gains and losses.

An investor can correctly identify a growing industry and still choose a company that performs badly because of:

- Poor leadership.

- Excessive debt.

- Fraud.

- Competition.

- Regulatory problems.

- Technological change.

- Overvaluation.

- Product failure.

Holding an individual stock is different from owning a broad fund.

A diversified fund can survive the failure of one company because it holds many others. A concentrated portfolio may suffer permanent damage from one mistake.

Wealthy investors who purchase individual companies may have access to:

- Professional research.

- Financial advisers.

- Industry knowledge.

- Management teams.

- Risk controls.

- Large portfolios that support diversification elsewhere.

Ordinary investors should not assume that copying a billionaire’s publicly reported purchase will produce the same outcome.

The wealthy investor may have:

- Purchased at a different price.

- Hedged the position.

- Obtained special rights.

- Held other assets that offset the risk.

- Planned a much longer investment period.

- Sold before the public learns about it.

Individual shares can be legitimate investments, but they require research and the ability to tolerate permanent loss.

4. Income-producing property

Real estate is one of the most recognisable assets associated with wealth.

Income-producing property may include:

- Residential rental homes.

- Apartment buildings.

- Offices.

- Warehouses.

- Retail buildings.

- Student accommodation.

- Industrial facilities.

- Medical offices.

- Hotels.

- Agricultural land.

- Self-storage facilities.

Returns may come from:

- Rent.

- Property appreciation.

- Loan repayment by rental income.

- Property development.

- Renovation.

- Changes in land use.

Property can provide regular cash flow, but rent is not the same as profit.

Owners must subtract:

- Mortgage payments.

- Property taxes.

- Insurance.

- Repairs.

- Management fees.

- Vacancies.

- Legal expenses.

- Utilities.

- Security.

- Association charges.

- Transaction costs.

A property producing $3,000 in monthly rent may generate little profit after all expenses are included.

Why wealthy investors use property

Property may offer:

- Rental income.

- Potential appreciation.

- Access to borrowing.

- A tangible asset.

- Partial inflation protection.

- Portfolio diversification.

- Control over renovation and management.

Borrowing can magnify returns when prices and rent increase.

It can also magnify losses when values fall, interest rates rise or units remain vacant.

Property is not automatically passive

Landlords must deal with:

- Tenant screening.

- Late payments.

- Repairs.

- Local laws.

- Insurance.

- Contractors.

- Record keeping.

- Safety requirements.

Professional property managers can perform much of this work, but they charge fees.

Real estate can be profitable, but it should be evaluated as an operating business rather than a guaranteed source of easy monthly income.

5. Real estate investment trusts

A real estate investment trust, or REIT, is a company that owns or finances income-producing real estate.

Investor.gov describes a REIT as a company that typically owns and operates income-producing properties or related assets.

REITs allow investors to gain property exposure without personally buying and managing an entire building.

Depending on the REIT, it may invest in:

- Apartments.

- Warehouses.

- Shopping centres.

- Hotels.

- Data centres.

- Mobile towers.

- Hospitals.

- Offices.

- Mortgage assets.

- Self-storage facilities.

Publicly traded REITs can often be bought and sold through brokerage accounts like ordinary shares.

Why wealthy investors use REITs

REITs can provide:

- Property income.

- Professional management.

- Diversification across properties.

- Easier buying and selling than direct property.

- Access to large commercial assets.

- Dividend distributions.

A person may be unable to buy a major warehouse or data centre directly but may purchase shares in a company that owns many such buildings.

Main REIT risks

REIT prices may fall because of:

- Rising interest rates.

- Falling property demand.

- Weak rental income.

- Excessive debt.

- Property oversupply.

- Poor management.

- Economic recessions.

- Changes in remote working or retail behaviour.

Not every REIT is publicly traded.

Non-traded REITs may have high fees, limited liquidity and complicated redemption restrictions. Investors should understand exactly how and when their money can be withdrawn.

6. Government and high-quality bonds

A bond is a form of lending.

When an investor purchases a bond, the investor lends money to a government, company or other organisation. In return, the issuer generally promises interest payments and repayment of principal under stated conditions.

Wealthy investors often use bonds for:

- Income.

- Capital preservation.

- Diversification.

- Liquidity.

- Reducing portfolio volatility.

- Matching future financial obligations.

Bonds are generally considered less volatile than stocks, but they are not risk-free.

Bond risks

Bond investors can face:

- Interest-rate risk.

- Inflation risk.

- Credit risk.

- Currency risk.

- Liquidity risk.

- Reinvestment risk.

- Early repayment.

- Default.

When market interest rates rise, existing fixed-rate bonds often fall in value because newly issued bonds may offer higher yields.

A bond paying 3% becomes less attractive when similar new bonds pay 5%.

An investor who holds a high-quality bond until maturity may receive the promised principal, assuming the issuer remains able to pay. An investor who must sell early may experience a loss.

Why wealthy people still hold bonds

The objective is not always maximum growth.

Someone who has already accumulated substantial wealth may place greater importance on preserving capital and producing predictable income.

A diversified portfolio may therefore include both growth assets and more defensive assets.

Investor.gov identifies stocks, bonds and cash as the three main asset classes and states that the appropriate allocation depends on the investor’s circumstances.

7. Cash and short-term instruments

Cash is often criticised because inflation reduces its purchasing power.

However, wealthy people still hold cash and cash-like assets.

The purpose is not necessarily long-term growth.

Cash provides:

- Liquidity.

- Emergency protection.

- Flexibility.

- Funds for taxes.

- Money for planned purchases.

- The ability to invest during market declines.

- Protection from being forced to sell other assets.

Cash-like assets may include:

- Regulated savings accounts.

- Fixed deposits.

- Treasury bills.

- Money-market funds.

- Short-term government securities.

These products have different risks and protections. A money-market fund is an investment and should not automatically be treated as an insured bank deposit.

The opportunity value of cash

Suppose property prices or stock markets fall significantly.

An investor with available cash may purchase assets at lower prices.

An investor with no liquidity may be forced to sell during the decline to pay bills.

This is why cash can be strategically valuable even when its expected return is lower than that of long-term assets.

The main danger of excess cash

Holding too much money in low-return accounts for decades can lead to purchasing-power loss.

The correct amount depends on:

- Monthly expenses.

- Income stability.

- Planned purchases.

- Business risks.

- Investment opportunities.

- Personal comfort.

- Access to other sources of liquidity.

Cash is not useless.

It is an asset with a specific purpose and a significant long-term inflation risk.

8. Intellectual property

Intellectual property is an asset created through ideas, creativity, knowledge or innovation.

Examples include:

- Books.

- Music.

- Films.

- Software.

- Patents.

- Trademarks.

- Designs.

- Courses.

- Photography.

- Research.

- Media archives.

- Characters.

- Proprietary systems.

Intellectual property can generate money through:

- Licensing.

- Royalties.

- Subscriptions.

- Advertising.

- Product sales.

- Franchising.

- Distribution rights.

The powerful feature of intellectual property is scalability.

A physical service may need to be performed separately for each customer. A digital product can potentially be sold repeatedly after it has been created.

However, this does not make revenue automatic.

A book can sell no copies. Software can become outdated. A patent may be expensive to defend. A course can lose relevance. A media platform can change its algorithm.

What makes intellectual property valuable?

Value may depend on:

- Demand.

- Legal ownership.

- Quality.

- Uniqueness.

- Distribution.

- Brand recognition.

- Marketing.

- Remaining protection period.

- Ability to prevent unauthorised use.

- Potential to generate repeat income.

Wealthy business owners often separate intellectual property from day-to-day operations because copyrights, trademarks and software may remain valuable even if the original business model changes.

Content creators can also build intellectual-property assets through original articles, videos, photography, newsletters and educational products.

The key word is original.

Copying another creator’s work does not build a defensible asset and can create legal liability.

9. Professional skills and education

Skills are sometimes overlooked because they do not appear in an investment account.

However, a valuable skill can increase income for decades.

Examples include:

- Software development.

- Engineering.

- Sales.

- Accounting.

- Healthcare.

- Financial analysis.

- Communication.

- Management.

- Media production.

- Digital marketing.

- Skilled trades.

- Data analysis.

- Entrepreneurship.

Education becomes an asset when it improves the ability to produce valuable work.

It becomes an expense when it is purchased without considering:

- Demand.

- Cost.

- Completion probability.

- Expected income.

- Alternative training.

- Time required.

- The quality of the provider.

A prestigious qualification can still produce a weak financial return when financed with excessive debt or pursued in a field with limited opportunities.

Similarly, an inexpensive technical certification can be highly valuable when it leads directly to in-demand work.

Why wealthy people continue learning

People with substantial resources often purchase:

- Specialist training.

- Professional advice.

- Coaching.

- Industry research.

- Conferences.

- Technical certifications.

- Books.

- Access to expert networks.

The aim is not simply collecting certificates.

The aim is improving judgment, income, leadership and access to opportunities.

Skills can also protect a person when other assets fall. Someone with valuable expertise may be able to rebuild income after a business failure or market decline.

10. Private companies and alternative assets

Wealthy and institutional investors sometimes purchase assets that are not easily available through ordinary public markets.

These can include:

- Private companies.

- Venture capital.

- Private credit.

- Infrastructure.

- Farmland.

- Timber.

- Collectibles.

- Precious metals.

- Private real estate.

- Limited partnerships.

Investor.gov lists real estate, precious metals, commodities and private equity among alternative asset categories, while warning that each carries category-specific risks.

Private equity involves ownership in companies that are not publicly traded.

Private credit involves lending outside traditional public bond markets.

Infrastructure can include:

- Energy systems.

- Transport.

- Communications networks.

- Utilities.

- Data facilities.

Why wealthy investors use alternatives

Alternative assets may provide:

- Different sources of return.

- Income.

- Diversification.

- Exposure to businesses before public listing.

- Partial inflation protection.

- Access to specialised opportunities.

However, alternatives can be extremely risky.

They may involve:

- High fees.

- Long lock-up periods.

- Limited information.

- Difficult valuations.

- Large minimum investments.

- Manager dependence.

- Legal complexity.

- Complete loss of capital.

Private investments are not automatically superior because they are exclusive.

Sometimes exclusivity simply makes an investment harder to evaluate and harder to sell.

Ordinary investors should be especially cautious when someone promotes an unlisted investment using words such as “private,” “elite” or “institutional” as proof of quality.

Assets wealthy people do not necessarily buy

Wealth is often marketed through visible consumption.

Advertisements may suggest that rich people constantly buy:

- Luxury cars.

- Designer clothes.

- Watches.

- Boats.

- Large homes.

- Private travel.

Some wealthy people purchase these items, but they are not automatically productive assets.

A personal vehicle usually declines in value. A luxury home may create high taxes and maintenance expenses. Designer products may have limited resale value.

An expensive item becomes an investment only when there is a realistic way to generate an economic return or preserve value.

A luxury purchase can still be enjoyable.

It should simply be classified honestly as consumption rather than wealth creation.

What makes something an asset?

An asset may provide one or more of four benefits.

Income

It produces rent, interest, dividends, royalties or business profit.

Appreciation

Its value may increase over time.

Utility

It reduces expenses or enables valuable work.

Strategic value

It provides liquidity, control, legal rights or access to future opportunities.

The presence of one benefit does not make the asset suitable.

A rental property may produce income but require too much debt. A stock may have growth potential but be dangerously overpriced. A skill may increase income but cost too much to acquire.

Every asset should be evaluated according to:

- Expected return.

- Risk.

- Time horizon.

- Liquidity.

- Fees.

- Taxes.

- Required expertise.

- Diversification.

- Personal objectives.

Income-producing assets versus appreciating assets

Some assets are purchased mainly for income.

Examples include:

- Bonds.

- Rental property.

- Dividend-paying shares.

- Income funds.

- Private loans.

Other assets are purchased mainly for growth.

Examples may include:

- Growth companies.

- Development land.

- Early-stage businesses.

- Intellectual property.

- Certain commodities.

Many assets can provide both income and appreciation.

A rental property may generate rent and rise in value. A company may pay dividends and increase its share price.

The right combination depends on the investor’s needs.

A younger investor with stable employment may prioritise growth.

Someone relying on investments to pay living expenses may prioritise income, liquidity and capital preservation.

Why diversification matters

Wealthy people rarely depend on one asset because every asset can fail.

A business can lose customers.

A property can remain vacant.

A stock can collapse.

A bond issuer can default.

Cash can lose purchasing power.

Intellectual property can become outdated.

Diversification spreads exposure across different investments and economic conditions.

Investor.gov states that diversification may reduce the risk of severe loss but cannot guarantee that a portfolio will avoid declines.

Diversification should exist:

- Across asset classes.

- Within asset classes.

- Across industries.

- Across locations.

- Across currencies where appropriate.

- Across income sources.

- Across time.

Owning 20 technology companies is not the same as owning a diversified portfolio when they respond to the same economic risks.

The role of tax-advantaged accounts

An asset can produce different results depending on the account in which it is held.

Some countries provide retirement, education or investment accounts with tax advantages.

In the United States, traditional and Roth individual retirement arrangements allow eligible investors to receive specific tax benefits. The IRS states that IRAs are designed to support tax-advantaged retirement investing.

For 2026, the standard contribution limit for 401(k), 403(b), most 457 plans and the federal Thrift Savings Plan is $24,500. The general IRA limit is $7,500, subject to eligibility and income rules.

These figures apply to the United States and may change.

Other countries have different pension and investment systems.

Tax advantages do not make a poor asset attractive, but they can improve the long-term result of a suitable investment.

Investors should understand:

- Contribution limits.

- Withdrawal restrictions.

- Tax treatment.

- Employer contributions.

- Penalties.

- Investment options.

- Beneficiary rules.

Why fees matter

Wealthy investors often pay close attention to fees because small percentages become large amounts over time.

Common costs include:

- Fund expense ratios.

- Brokerage fees.

- Adviser charges.

- Property management.

- Legal expenses.

- Performance fees.

- Trading spreads.

- Platform charges.

- Insurance.

- Taxes.

Consider $100,000 growing at 7% annually for 30 years.

Without fees, it would grow to approximately $761,000.

At a net return of 6% after an additional 1% annual cost, it would grow to approximately $574,000.

The difference is about $187,000.

This is a simplified example, but it demonstrates how recurring costs compound.

A higher-fee investment may be justified when it provides genuine specialised value.

The investor should still understand the complete cost.

Liquidity can be more important than return

Liquidity describes how easily an asset can be converted into cash without a major price reduction.

Publicly traded shares can often be sold quickly during market hours.

A property may take months to sell.

A private company investment may be locked for many years.

A valuable patent may have no immediate buyer.

An investor with substantial illiquid wealth can still face financial difficulty when cash is needed urgently.

This is why portfolios often include liquid reserves alongside long-term assets.

A high expected return is not useful when the investor must sell at a large discount during an emergency.

The danger of borrowing to buy assets

Borrowing can accelerate wealth creation.

It can also accelerate bankruptcy.

A mortgage allows someone to control a property worth much more than the down payment. Business loans can finance expansion. Investment credit can increase market exposure.

This is known as leverage.

Suppose an investor contributes $20,000 and borrows $80,000 to purchase a $100,000 asset.

If the asset rises to $110,000, the $10,000 gain represents 50% of the original equity before costs.

If the asset falls to $90,000, the $10,000 loss represents 50% of the original equity.

Debt payments continue even when income or asset values decline.

Leverage should be evaluated according to:

- Interest rate.

- Repayment schedule.

- Income stability.

- Collateral.

- Worst-case losses.

- Ability to survive vacancies or market declines.

Rich people may use debt strategically, but they can also lose enormous fortunes through excessive leverage.

How ordinary people can begin buying assets

Building assets does not require purchasing an apartment building or private company immediately.

A practical sequence may include:

- Establishing a basic emergency fund.

- Paying high-cost consumer debt.

- Using available employer retirement contributions.

- Learning the basics of diversified investing.

- Beginning with regulated, low-cost products.

- Increasing contributions as income rises.

- Building skills that improve earning power.

- Avoiding investments that are not understood.

- Diversifying gradually.

- Reviewing progress regularly.

A small asset purchased consistently can become meaningful through time and compounding.

The starting amount matters less than:

- Consistency.

- Fees.

- Time.

- Risk control.

- Avoiding major permanent losses.

Someone investing $100 every month is building an asset habit.

Someone waiting for enough money to make one dramatic investment may never begin.

Questions to ask before buying any asset

Before investing, ask:

- How does this asset generate a return?

- What could cause me to lose money?

- How quickly can I sell it?

- What fees will I pay?

- What taxes may apply?

- Is it regulated?

- Who controls the asset?

- Can I verify ownership?

- Does the promised return match the risk?

- How does it fit with my other assets?

- When will I need the money?

- What happens in a recession?

- Am I buying because of research or social pressure?

- Can I tolerate a major decline?

- Is borrowing involved?

An investment should not depend on secrecy, urgency or recruiting new participants.

Warning signs of fake assets and investment fraud

Fraudsters often copy the language of legitimate wealth building.

They may promote:

- Guaranteed monthly returns.

- Secret investment systems.

- Exclusive opportunities.

- Artificially urgent deadlines.

- Unlicensed property schemes.

- Fake shares.

- Unregistered funds.

- Businesses with no verifiable revenue.

- Digital tokens with no clear purpose.

- Investments that reward recruitment.

A high return with little or no risk is a major warning sign.

Before investing, verify:

- The company.

- The seller.

- The regulator.

- The legal documents.

- The asset’s existence.

- Withdrawal conditions.

- Independent financial records.

Do not rely only on screenshots, testimonials or visible displays of wealth.

A person renting luxury cars for social media can appear richer than an investor quietly holding diversified assets.

Common misconceptions

“Rich people only buy property”

Many wealthy portfolios include businesses, stocks, bonds, cash and intellectual property.

“Every asset produces passive income”

Most assets require research, management or monitoring.

“A personal home is always an investment”

A home can build equity, but it also produces taxes, interest, insurance and maintenance expenses.

“Dividends are free money”

A dividend is paid from company resources, and the share price can still decline.

“Private investments are better than public markets”

Private assets may be illiquid, expensive and difficult to value.

“Debt is always bad”

Debt can finance productive assets, but excessive leverage can destroy wealth.

“Cash is not an asset”

Cash provides liquidity and stability, although inflation may reduce its purchasing power.

“You need to be rich before buying assets”

Many diversified funds and savings products allow relatively small contributions.

“Wealthy investors never lose”

Every successful investor experiences poor investments, market declines or business setbacks.

Future outlook

The range of assets available to individual investors is expanding.

Digital platforms increasingly offer access to:

- Fractional shares.

- Government securities.

- Property funds.

- Private-market products.

- Automated portfolios.

- International markets.

This accessibility can be useful, but it can also expose inexperienced investors to complex and illiquid products.

Investor.gov’s 2026 guidance continues to emphasise that asset allocation should reflect personal time horizon and risk tolerance, while diversification can reduce—but not eliminate—risk.

Technology may make investing faster.

It does not make due diligence less important.

Artificial intelligence can help analyse financial information, but it can also be used to produce fake investment materials, fabricated endorsements and convincing scams.

The principles of wealth creation remain largely unchanged:

- Spend less than you earn.

- Protect against emergencies.

- Acquire productive assets.

- Diversify.

- Control fees.

- Avoid excessive debt.

- Think in decades rather than days.

Conclusion

Rich people do not all purchase the same assets.

Their portfolios depend on income, age, objectives, tax rules, business interests and risk tolerance.

However, many wealthy investors repeatedly direct money toward assets that can generate income, increase in value or support future opportunities.

These commonly include:

- Businesses.

- Diversified stock funds.

- Individual company shares.

- Income-producing property.

- Real estate investment trusts.

- Government and high-quality bonds.

- Cash and short-term instruments.

- Intellectual property.

- Professional skills and education.

- Private companies and alternative assets.

The lesson is not to imitate every purchase made by a millionaire or billionaire.

Wealthy investors may have more information, more liquidity and a greater capacity to survive losses.

The better lesson is to move gradually from consumption toward ownership.

Before buying an asset, understand how it creates value, what it costs, when it can be sold and how much could be lost.

No asset is guaranteed.

The strongest wealth-building plan combines productive assets with emergency reserves, diversification, patience and responsible risk management.

Disclaimer: This article provides general financial education and does not constitute personalised investment, property, tax, legal or business advice. Investments can lose value, income is not guaranteed and past performance does not predict future results. Regulations and tax rules vary by jurisdiction. Consider official information and appropriately qualified advice before making significant financial decisions.

Read Also: The Psychology of Spending: Why We Buy More Than We Planned

Sources consulted

- Investor.gov — Beginner’s Guide to Asset Allocation, Diversification and Rebalancing

https://www.investor.gov/additional-resources/general-resources/publications-research/info-sheets/beginners-guide-asset - Investor.gov — Asset Allocation and Diversification

https://www.investor.gov/introduction-investing/getting-started/asset-allocation - Investor.gov — Diversify Your Investments

https://www.investor.gov/introduction-investing/investing-basics/save-and-invest/diversify-your-investments - Investor.gov — Learn About Investment Options

https://www.investor.gov/introduction-investing/investing-basics/save-and-invest/learn-about-investment-options - Investor.gov — Mutual Funds

https://www.investor.gov/introduction-investing/investing-basics/investment-products/mutual-funds-and-exchange-traded-funds-etfs/mutual-funds - Investor.gov — Real Estate Investment Trusts

https://www.investor.gov/introduction-investing/investing-basics/investment-products/real-estate-investment-trusts-reits - Investor.gov — Asset Classes

https://www.investor.gov/introduction-investing/investing-basics/glossary/asset-classes - Investor.gov — Investor Tips for 2026

https://www.investor.gov/introduction-investing/general-resources/news-alerts/alerts-bulletins/investor-bulletins/investorgov-tips-2026-investor-bulletin - Internal Revenue Service — Retirement Plans

https://www.irs.gov/retirement-plans - Internal Revenue Service — 2026 Retirement Contribution Limits

https://www.irs.gov/newsroom/401k-limit-increases-to-24500-for-2026-ira-limit-increases-to-7500 - Internal Revenue Service — Individual Retirement Arrangements

https://www.irs.gov/retirement-plans/individual-retirement-arrangements-iras - Internal Revenue Service — IRA Contribution Limits

https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-ira-contribution-limits

{kind=link}