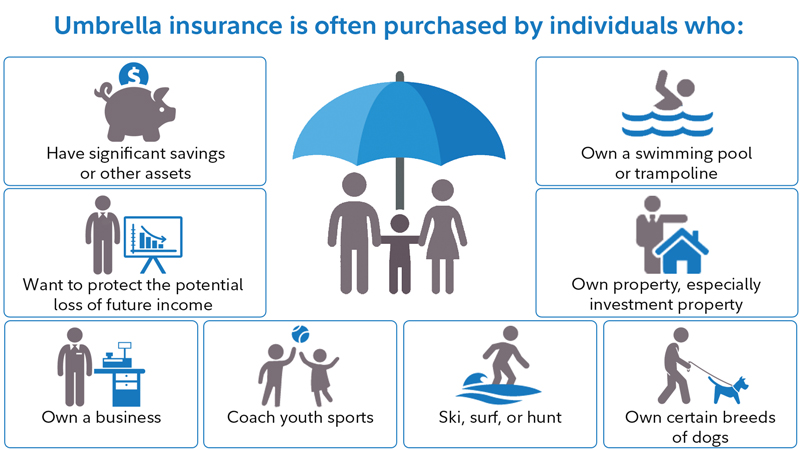

When it comes to protecting your wealth and future, few tools are as powerful—or as misunderstood—as umbrella insurance policies. These supplemental liability policies kick in when the limits of your home, auto, or other standard insurance are exhausted. In an era of rising lawsuits and settlement amounts, umbrella insurance can be the financial firewall that saves your assets from being wiped out by a single catastrophic event.

However, as with any type of insurance, umbrella policies aren’t for everyone. They provide significant advantages, but also come with costs, conditions, and limitations you should fully understand. Whether you’re a high-net-worth individual or simply want extra peace of mind, this article lays out the key pros and cons of umbrella insurance policies to help you make an informed decision.

✅ Pros of Umbrella Insurance Policies

1. Extended Liability Coverage

Umbrella insurance offers protection beyond your standard policy limits. If you’re sued for $1 million and your auto insurance only covers $300,000, your umbrella policy can cover the remaining $700,000—preventing you from having to pay out-of-pocket.

2. Broad Coverage Across Multiple Policies

It extends over various policies, including home, auto, boat, and rental property. This makes it a cost-effective way to boost protection across your entire insurance portfolio.

3. Legal Defense Costs Included

Most umbrella policies cover legal defense costs, even if the lawsuit is groundless. This includes attorney fees, court costs, and settlements, offering peace of mind during lengthy legal battles.

4. Affordable Premiums

For the level of protection it offers, umbrella insurance is surprisingly inexpensive—typically starting around $150 to $300 annually for the first $1 million in coverage.

5. Covers Uncommon Risks

Umbrella policies often include coverage for libel, slander, false arrest, or rental property liability—risks that are not always covered under basic home or auto insurance.

❌ Cons of Umbrella Insurance Policies

1. Requires High Base Coverage First

To qualify, insurers usually require that you carry high liability limits on your home and auto policies (e.g., $300,000 for home, $250,000/$500,000 for auto). This could mean additional premium costs before even adding an umbrella.

2. No Coverage for Your Own Losses

Umbrella insurance doesn’t pay for your injuries or damages—it only covers your legal liability to others. If you’re seeking coverage for your own property or medical expenses, this won’t help.

3. May Not Cover Business Activities

Standard umbrella policies typically exclude coverage for business-related claims unless you purchase a commercial umbrella policy. This can be a major limitation for freelancers or small business owners.

4. Exclusions Apply

Intentional acts, criminal activity, and certain high-risk hobbies (like racing or aviation) are generally excluded. Misunderstanding these exclusions could leave you vulnerable.

5. Complex Underwriting for High Coverage

If you’re seeking multi-million dollar umbrella limits, expect a more rigorous underwriting process, including income verification and asset documentation.

Final Thoughts

Umbrella insurance policies are a smart safeguard against financial catastrophe, especially in today’s litigious society. They offer substantial peace of mind at a low cost, especially for individuals with significant assets or public exposure. However, their true value depends on your financial situation, risk profile, and existing insurance coverage. By weighing the pros and cons, you can determine whether this extra layer of liability protection fits into your overall financial strategy.

{kind=link}